Originally published on Jan. 16, 2022 by TraderStef at CrushTheStreet

Fed Chairman Jerome Powell testified in front of Congress last week for a second-term confirmation and tiptoed around the Federal Reserve’s plan on tapering its accommodative monetary policy to “rate normalization” in 2022 and beyond. The barrage of questions about the global and domestic economy, taper planning, and policy matters from your elected officials on Capitol Hill was met with answers predicated by Fed speak safety nets that included “maybe,” “expect,” “willing to adapt,” “must be humble,” “depends on the data,” “we honestly don’t know,” and “no decisions made at this time.” There was no definitive answer to the requirements for a quickened taper and normalization. If you didn’t indulge the pleasure of partisan brown-nosing and fingernails on a chalkboard for two hours, have at it.

If you missed my humble opinion in Part 1 last summer, here is an excerpt:

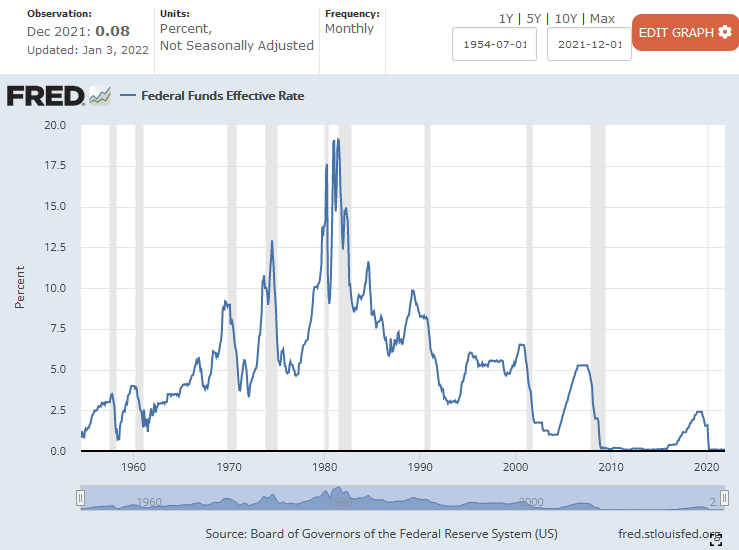

“Remember when Ben Bernanke finally walked the quantitative easing (QE) taper talk in Dec. 2013, six months after letting the cat out of the bag during his May 2013 congressional testimony that launched an infamous ‘taper tantrum?’ Remember when Janet Yellen pulled the interest rate trigger with a 0.25% piker in Dec. 2015 after seven long years of a near-zero interest rate (aka ZIRP) that followed the Great Financial Crisis, but not until Bernanke had already begun the attempt at normalization by scaling back QE3 and QE4? Yellen managed to raise rates up to 1.5% by Dec. 2017, and after Jay Powell became the Fed Chair in Feb. 2018, he hiked rates up to 2.5% by Dec. 2020. Then, the pandemic initiated explosive fiscal and monetary policies and a return to ZIRP with an effective Federal Funds Rate low of 0.06% in May 2021. As the new Treasury secretary for the Biden administration, Yellen managed to cause a small taper tantrum when she opined in early May that ‘interest rates will have to rise somewhat’ and promptly walked back those comments when the stock market tanked. In retrospect, it took 12 years to exit ZIRP and reach an ear-popping height of 2.5%, then only 3 months for the pandemic ZIRP to appear and thus far remain zero-bound.” – TraderStef

After 6 weeks of the Fed reducing monthly purchases of mortgage-backed securities and Treasuries, the Federal Funds Effective Rate clocked in at a whopping 0.08% as of Jan. 3, 2022.

The Fed Is Hawkish Now? I’ll Believe It When I See It… “In light of inflation developments and the further improvement in the labor market, the Committee decided to reduce the monthly pace of its net asset purchases by $20 billion for Treasury securities and $10 billion for agency mortgage-backed securities. Beginning in January, the Committee will increase its holdings of Treasury securities by at least $40 billion per month and of agency mortgage‑backed securities by at least $20 billion per month. The Committee judges that similar reductions in the pace of net asset purchases will likely be appropriate each month, but is prepared to adjust the pace of purchases if warranted by changes in economic outlook.” – Mises Institute, Dec. 17

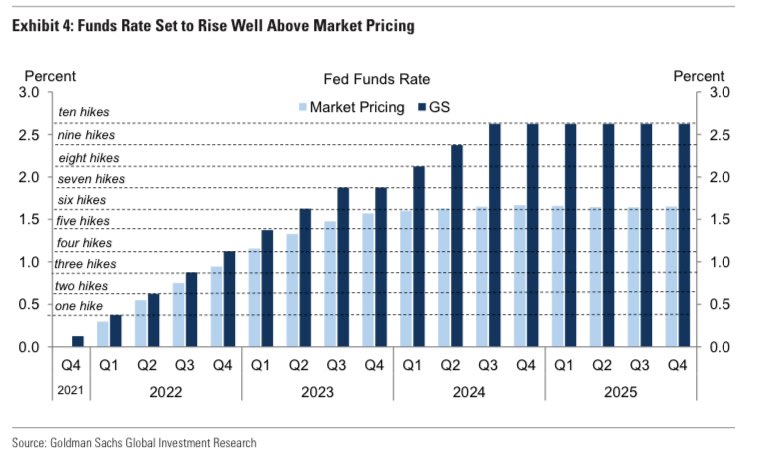

Fed’s Funds Rate Projected Increases 2022-2025:

Hints of an endless #TaperCaper reemerged in social media posts, the economic analysts’ blogosphere, among pandemic Zoomers at Wall Street banking institutions, hedge fund back-office chat, and buried within the mainstream financial press.

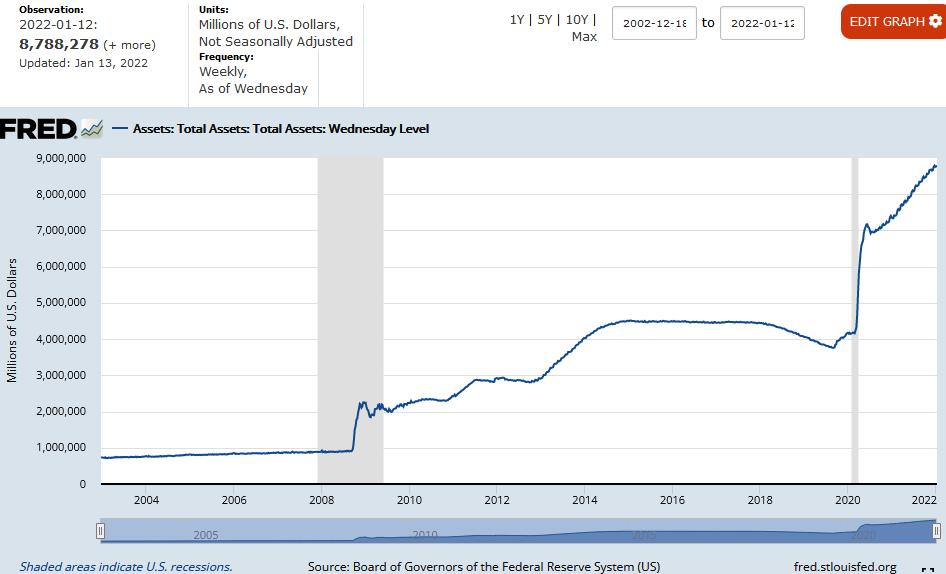

The Fed is about to see a lot of new faces. What it means for banks, the economy and markets… “The Fed also is expected to halt its monthly asset purchases in March. Where the board seems less decisive is on reducing some of the more than $8.8 trillion in assets the Fed is holding. Some officials at the December meeting said balance sheet reduction could start shortly after rate hikes begin, but others in recent days have expressed uncertainty about the process. ‘People want the Fed to do something about inflation. But as growth starts to slow around the spring, people aren’t going to want to pay higher borrowing costs,’ said Joseph LaVorgna, chief economist for the Americas at Natixis and chief economist for the National Economic Council under former President Donald Trump. ‘They’re going to be pretty dovish on the rates side, and may indeed push back on the balance sheet reduction,’ he added.” – CNBC, Jan. 15

Fallout in the global economy continues as multiple signals point to prolonged economic malaise heading into spring. China is in the midst of locking down millions in major cities as lockdowns are spreading throughout multiple provinces and the capital of Beijing, the Hong Kong and Shanghai international airports are shutting down cargo and commercial flights, shipping ports are reducing exports, and manufacturing hubs are experiencing renewed outbreaks.

Beijing is in a panic with the Winter Olympics slated to launch in early February. In addition to Delta and Omicron clusters, an outbreak of hemorrhagic fever is being downplayed by the CCP, and a new report suggests that China’s true death toll from the pandemic is 366x higher than officially reported. That report is not surprising and does not bode well for relying on what’s allowed to leak out about the current outbreaks and lockdowns. There will likely be a delay before more shipping hiccups impact the global supply chain that’s already in crisis mode.

The situation in the United States is not much better despite an outbreak of truth regarding the origins of the pandemic, mRNA gene therapy inoculations, adverse reactions leading to excess disabilities and death that can be attributed to vaccine tyranny, and the jabbed in other countries are filling up hospitals at 2x the rate of the unjabbed which invalidates U.S. propaganda. A high rate of Omicron infections is straining first responders and hospitals that fired staff due to mandates, private and small businesses are struggling or closing, and the labor force is battered by two years of intermittent lockdowns and restrictions.

There’s also the ongoing supply chain crisis and labor shortage within the U.S. that’s blatantly obvious with shortages of food and bare shelves at your local grocery chain, and employment across all industries has been impacted to some degree by a vaccine mandate that the Supreme Court finally struck down. Although, a trucking strike is now taking place due to new vaccine mandates imposed upon truckers crossing the U.S. Canadian border in either direction that will impact numerous supply chains. The healthcare industry is not covered by the current SCOTUS ruling, and some corporations and cities continue enforcing tyrannical mandates with impunity. Impacts from the issues noted above, along with inflation and lukewarm or contracting economic data, are weighing heavily on a fragile economic recovery.

In addition to an ongoing supply chain crisis and pandemic issues, several geopolitical hotspots are not going away, and Russia vs. NATO over Ukraine took the spotlight in recent days when talks collapsed with no sign of a restart. If diplomacy is not re-engaged immediately and efforts made by all sides to make concessions, a major outbreak in the Balkans or elsewhere will only increase stress on global supply chains as the potential for WWIII takes over the mainstream media. Imagine a new Cuban missile crisis in the near future while China, North Korea, and Iran take advantage of diplomatic and military weakness to freely embark upon their own agendas.

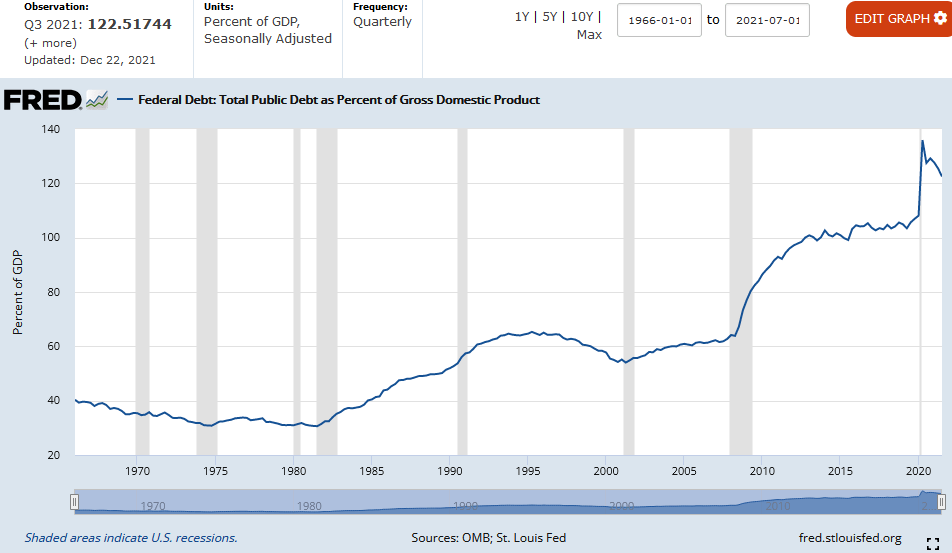

The release of less-than-positive economic data indicates that U.S. consumer price inflation climbed at the fastest pace in 39 years, retail sales are rolling over, and real wages continue to plummet on top of everything else. The odds of the Fed prancing to a happy ending with its taper strategy are not a horse I would bet on now. China’s central banking horse has already left the barn by cutting a key interest rate due to a slowdown in economic growth and liquidity issues. No matter what the Fed manages to pull off if geopolitical tensions and the pandemic subside, with a Federal Reserve balance sheet of $8.8 trillion and a national debt just shy of $30 trillion at 122% of GDP, the U.S. cannot afford interest rates beyond 2-3%, and even that number is pushing it because consumers would be crushed with financing debts.

If you’re procrastinating, get your house and portfolio in order now and stock your pantry with bullion, beans, and bullets before the supply gets tighter and prices go higher. There is always the possibility that things calm down and some semblance of normalcy returns, but prudence currently rules the day more than ever in the near term.

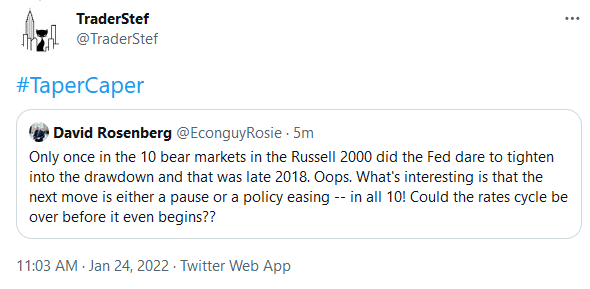

UPDATE Jan. 24, 2022…

Guns N’ Roses – Yesterdays

Plan Your Trade, Trade Your Plan

TraderStef on Twitter , Gab , Gettr / Website: TraderStef.com

Headline Collage Art by TraderStef

NONE of the content produced by TraderStef, staff members, or any services associated with this website should be construed as financial or investment advice. Financial investment is a risky endeavor and may lead to substantial loss. Always perform due diligence before undertaking any financial decision. Not a Financial Advisor. Copyrighted Material – A “by TraderStef” credit linked back to this website is required when using any quotes, written material, technical analysis charts, or publishing a full version of an article.

2 thoughts on “Another Taper Caper in a Ravenous World – Part 2”

Comments are closed.