Published First at CrushTheStreet Mar. 2024

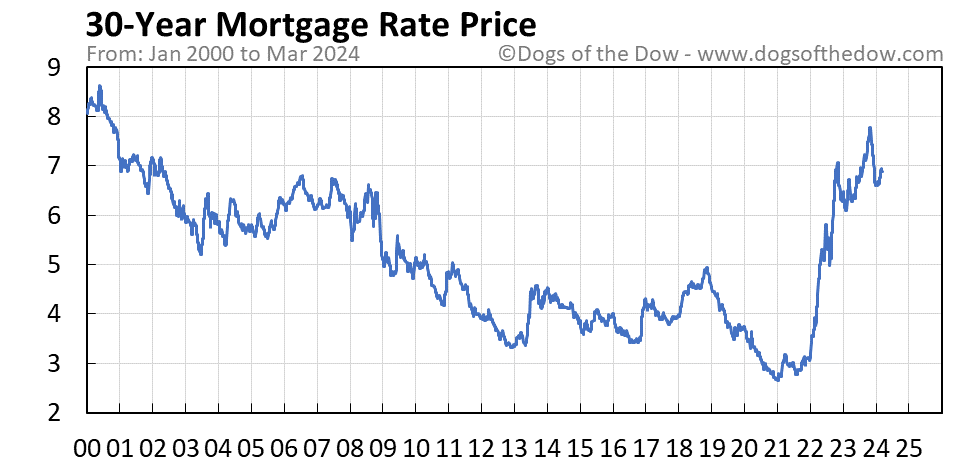

Elevated pricing for existing residential homes has been resilient overall despite the uptick in active listings YoY since summer 2023. Inventory did not increase until a year after the Federal Reserve launched an aggressive phase of quantitative tightening (QT) monetary policy and began raising interest rates in spring 2022 that peaked at 7-8% in fall 2023. Redfin released a report at the end of Feb. 2024 with a deep dive into housing statistics by region, median asking price, sale price, mortgage data, and inventory trends.

Data from Realtor.com last month “includes the active inventory of existing single-family homes and condos/townhomes/rowhomes/co-ops for the given level of geography. New construction is excluded unless listed via an MLS that provides listing data.” The report indicated that listings were up 14.8% YoY on a monthly basis and 19.9% YoY on a weekly one. New listings have increased YoY for 19 consecutive weeks. The 2023 winter season has steadily held onto the highest level of home listings since 2021 but is still down about 40% compared to the 2017-2020 pre-pandemic level. Inventory will need to rise quickly for any significant decline in asking prices as we head deeper into the buying season. An anticipated cut in interest rates by the Fed before summer sets in may be a catalyst for larger inventories, but any substantial reduction in mortgage financing will not manifest until late 2024 to 2025.

Inventory has also increased in the multifamily residential market due to a glut of construction in the pipeline. A report from Avison Young (PDF version) for 4Q23 showed there was a 14.6% increase in multifamily inventory since 2020, 50% of the top U.S. markets saw effective rents fall, and there was a 14.5% decline in average sale prices in 2023.

Excerpt from the CRE implosion:

“If you are looking to buy over the next year, keep a close eye on existing home inventory for a signal that a decline in home prices is likely to accelerate. A recent Bloomberg analysis on the effect 7-8% mortgage rates will have on the housing market noted that ‘we have to become super-focused on this low inventory, this low supply environment, because a growth in supply for any reason will lead to weakness in home prices.’” – TraderStef, Oct. 2023

Prices in residential housing will eventually come under pressure with help from “The Commercial Real Estate (CRE) Implosion – Part 4: Derivatives” (Twitter thread) going forward, which is deteriorating financial conditions for an unknown number of regional banks. Financing in the CRE sector includes multifamily housing, and regional banks financed a majority of CRE loans and mortgages when interest rates were historically low. That confluence may hasten contagion and worsen a banking crisis that found respite due to FDIC and Federal Reserve intervention during the collapse of Silicon Valley Bank, Signature Bank, and First Republic Bank last spring, which are three of the largest bank failures in history.

The FDIC released a Quarterly Banking Profile report for 4Q23 that includes a myriad of data points. One standout is net income for the 4,587 FDIC-insured commercial banks and savings institutions that declined $30 billion (43.9%) compared to 3Q23.

CRE a problem with heavy exposure to regional banks – Yahoo Finance, Feb. 8

NYCB’s latest woes spell out trouble for US banking sector – Yahoo Finance, Mar. 7

US Government’s ‘Problem Bank List’ Grew Again Last Quarter… “Washington’s ‘Problem Bank List’ rose again last quarter, capping off a year when US lenders struggled to cope with higher interest rates and more overdue loans for commercial buildings and credit cards. The FDIC said that its confidential tally of lenders with financial, operational, or managerial weaknesses had grown by eight banks to 52. The total assets held by those firms increased by $12.8 billion last quarter to $66.3 billion… The FDIC now estimates $20.4 billion in losses arising from the failure of both SVB and New York-based Signature Bank… Late payments on commercial properties that aren’t owner occupied are at the highest level since the first months of 2014, Gruenberg, the FDIC chairman, said in his remarks. Delinquent credit cards haven’t been this high since the third quarter of 2011, he added.” – Bloomberg, Mar. 7

Brokers in the housing market expect this spring’s home-buying season to remain a seller’s market. House hunters who have the capital, income, and credit worthiness to purchase are dealing with the confluence of high mortgage rates, sticky prices, and lackluster inventory that all contribute to warping the dynamics in real estate markets. Inventory is the main sticking point, especially for those seeking a well-maintained single-family home that’s not a fixer upper. Cash is king in all transactions, and provides some negotiating leverage if you have sufficient savings or liquid funds available. But even when a home hits the market in excellent condition and located within an ideal location, bidding wars are taking place, and most prospective buyers prefer not to or cannot afford to participate. Current buying conditions are reminiscent of bubble activity in the past, which includes the home hunting frenzy by folks exiting metropolises that frantically moved to the exurbs or remote rural areas during the pandemic panic.

The recent increase of inventory in certain regional markets might initiate a shallow pricing thaw this spring and summer, although a lot of homeowners will not give up a low interest rate on a current mortgage and take on a higher debt load with the increase in interest rates. The consumer misery index indicates that Bidenomics is a failure in an economy that’s nowhere near as peachy as some politicos and pundits claim. A good old-fashioned recession appears to be where the U.S. is headed and will do wonders for lowering home prices. Metro areas where new listings rose by around 50% in February vs. January were Minneapolis, Seattle, and Austin, Texas. Note that new home construction is experiencing a form of shrinkflation by building smaller houses that are more viable for buyers and builders.

Meanwhile, U.S. citizens are no longer leaving their metropolis due to a pandemic, but are fleeing liberal infernos cursed by socialist policies, high taxes, a crime wave, and low quality of life to instead live among law and order in conservative leaning states and cities. Adding insult to injury is the border crisis with examples of insane fiscal policies in sanctuary cities while they descend into chaos and bankruptcy. California is giving away free home loans to illegal aliens and New York hands out thousands of dollars in pre-paid cash cards on top of social welfare bennies already given, while U.S. citizens and veterans remain homeless or are evicted from homes so illegal immigrants can have “three-hots-and-a-cot” and a free apartment or hotel room.

Inside Mayor Adams’ migrant debit card boondoggle… “This debit card program — if you read the actual contract — has the potential to become an open-ended, multibillion-dollar Bermuda Triangle of disappearing, untraceable cash, used for any purpose. It will give migrants up to $10,000 each in taxpayer money with no ID check, no restrictions, and no fraud control.” – NYP, Feb. 19

Don’t expect residential property to flood markets in the near-term, but if you conduct due diligence to locate a home that meets needs instead of wants, there may be a house waiting for you as 2024 unfolds.

Barry Sternlicht on Regional Banks and Real Estate – Bloomberg, Feb. 22

Plan Your Trade, Trade Your Plan

Not a Financial Advisor: None of the content produced by TraderStef™, staff members, or any services associated with this website should be construed as financial or investment advice. Financial investment is a risky endeavor and may lead to substantial loss. Always perform due diligence before undertaking any financial decision – Copyrighted Material: A “by TraderStef” credit linked back to this website is required when using any quotes, technical analysis charts, or publishing a partial version of an article.

You must be logged in to post a comment.